2015: Analysis of Venture Capital, IPO & Exit Trends

2016 is turning out to be a tough year for startups and the venture capital industry. It shouldn’t come as a susrpise, for there were early signs of the coming slowdown – except no one was noticing.

With help of my friend Nima Wedake, I parsed the 2015 data from Pitchbook and other data sources to present a complete picture of funding and exit landscape.

You could see that all the hype around unicorns and their go-go valuations, was hiden the truth: Silicon Valley, like rest of industry can’t defy gravity forever.

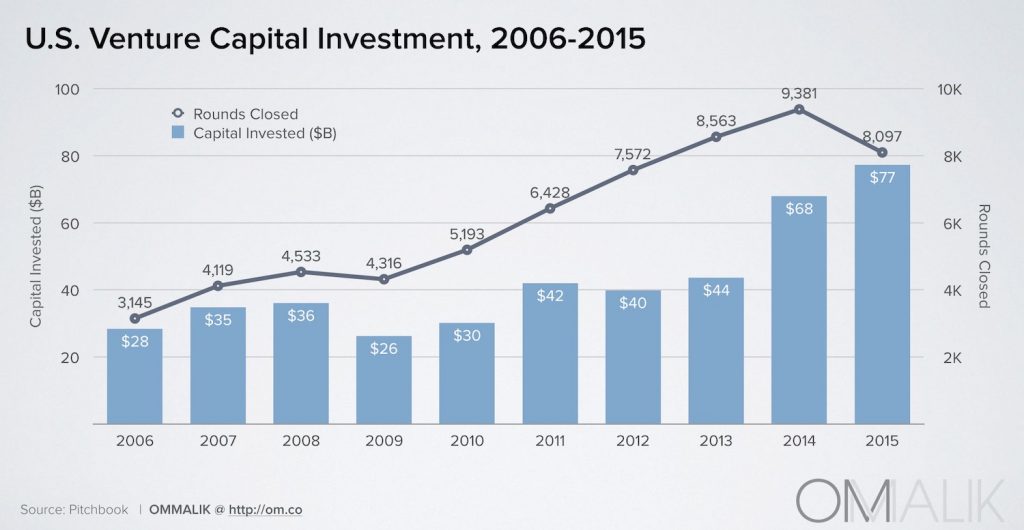

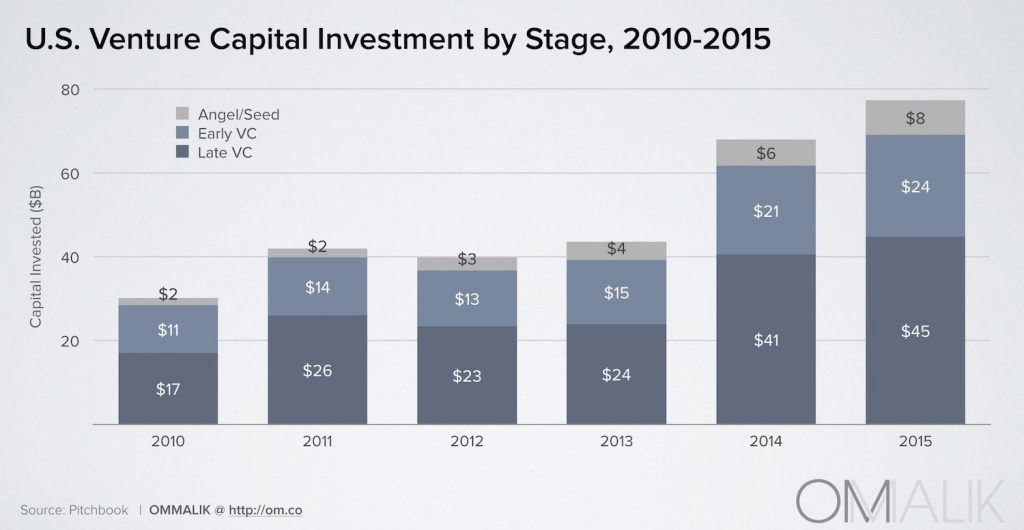

Total Capital Raised is up, but total # of deals is down

- Implication = Large late-stage rounds driving up the total $ amount (e.g Uber, Lyft, Airbnb, Snapchat, Zenefits, Pinterest)

- Average deal size for late stage rounds was up ~2.5x compared to 2010

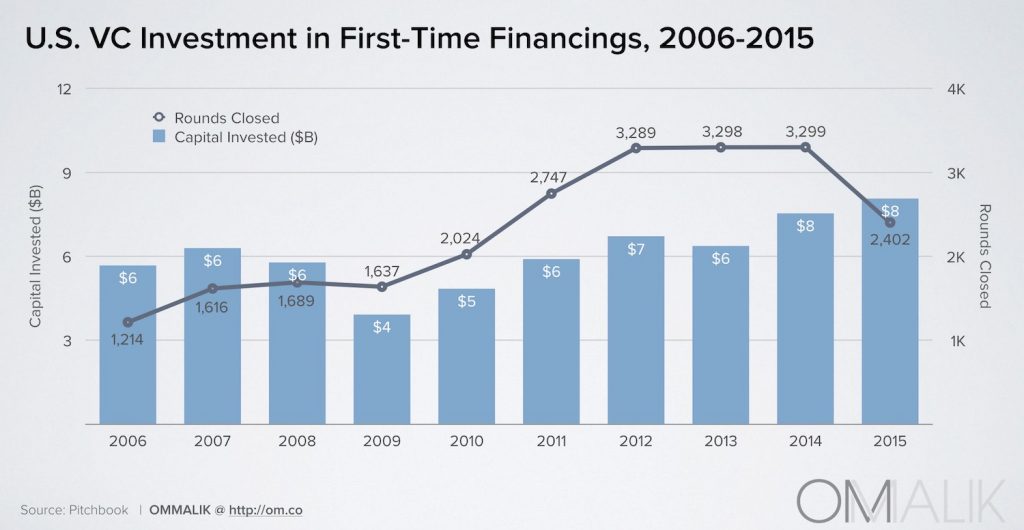

Sharp decline in the number of companies raising first-time funding

- Lowest level (2,042) since 2011

- Indicator of overall investor confidence

- Implication = placing bigger bets on later-stage companies with demonstrated traction.

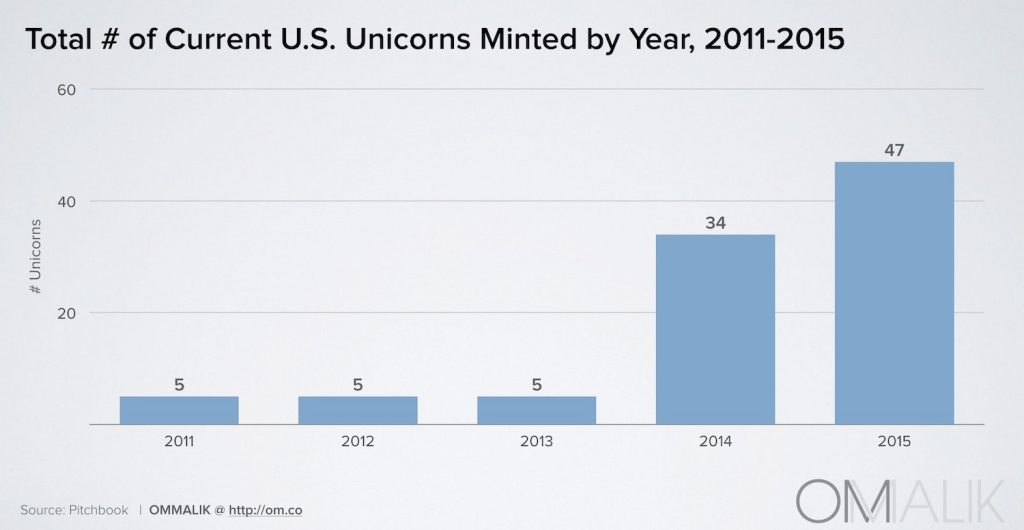

More Unicorns minted this year than the previous 4 years combined

- Implication = further evidence that “bets” are being placed on later stage companies; also an indicator of non-traditional funding sources (i.e. Fidelity investing in Snapchat)

- As we have seen lately, mutual funds can drive up (and drive down valuations.)

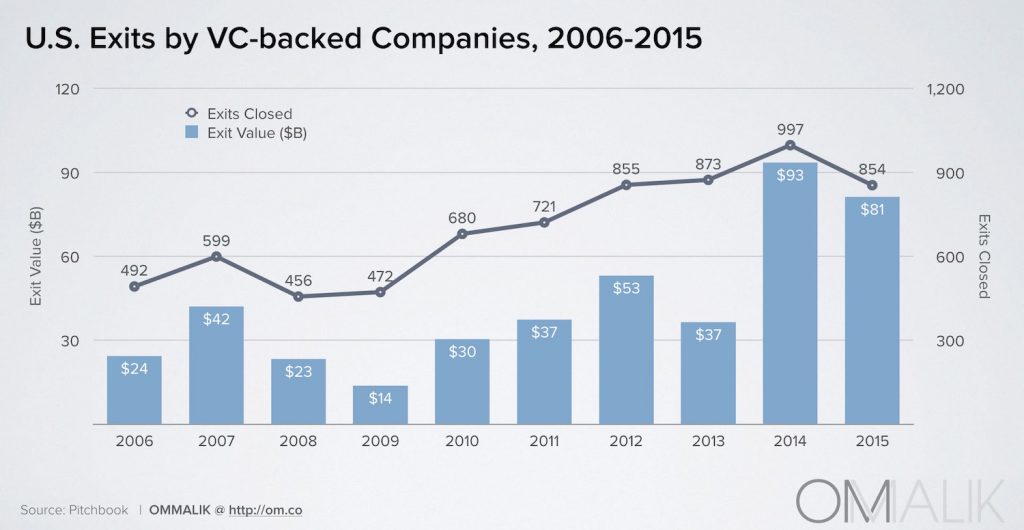

Slight decline in exits by VC-backed companies compared to 2014

- Still strong relative to previous years.

- Implications = Still an active M&A market, and many predict 2016 will be a years of increased acquisitions (see this post by Redpoint partner Tom Tunguz)

Worst year for technology IPOs since 2009

- Companies that do go public are getting beaten up (i.e. Etsy)

- The total volume of all the tech IPOs was $9.4 billion.

- Altogether, just five Unicorns went public in 2015. They include Box (in January), Shopify (May), Pure Storage (October), Square (November), and Atlassian (December) as seen here on the CrunchBase Unicorn Leaderboard.

- Implication = with recent market volatility, will be interesting to see the fate of Unicorns minted in the last few years. Will private capital still be available to them? Will we see several acquisitions in 2016 similar to the recent Gilt acquisition?

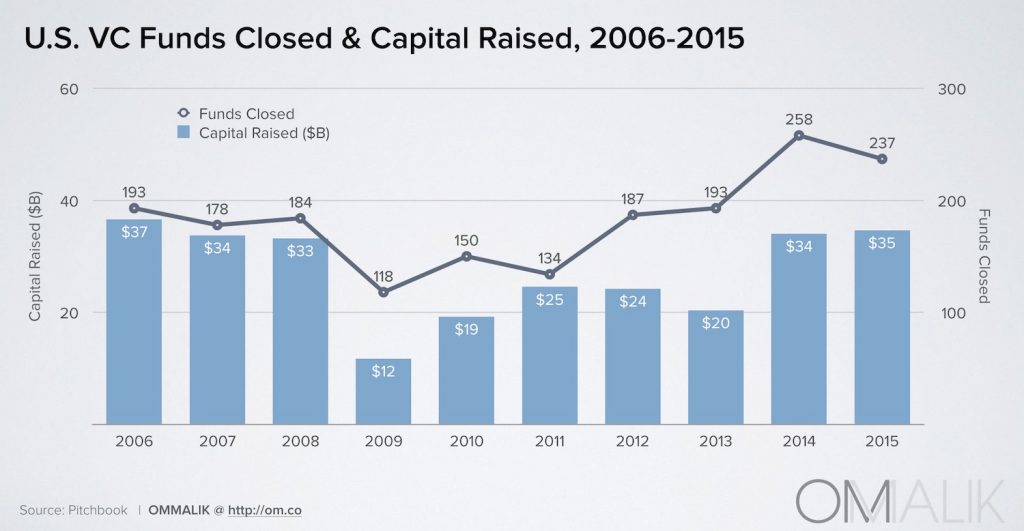

Most VC fundraising since 2006

- Implication = money still being poured into this asset class; still perceived as a place to chase returns