Pandemic will change money

The horrors of the pandemic are hard to ignore. The long-term damage to society is still unknown. What is undeniable, however, is that we are in a period of extreme, rapid change that will redefine how we interact with the world around us.

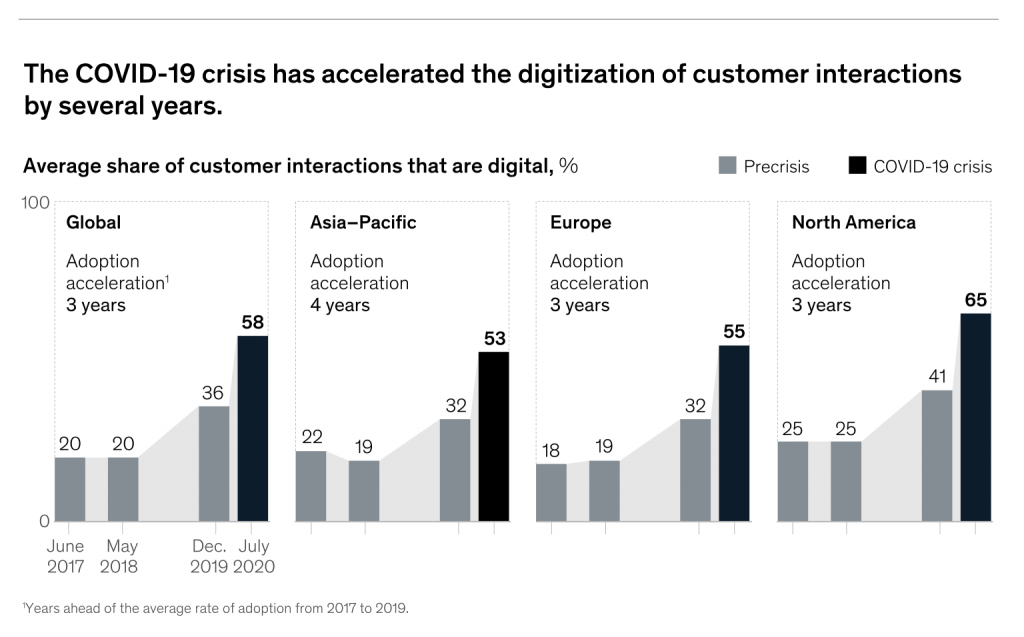

It has been said before and bears repeating: The pandemic has forced us into the future, and it has done so in a hurry. “The pandemic has compressed what might have taken 5 or 10 years, and it’s compressed it into a very, very short window,” Levi Strauss & Co. CEO Chip Bergh recently commented. McKinsey’s findings confirm as much. Selligent, a market company, surveyed 5,000 consumers in North American and Europe and found 36 percent of respondents shop online weekly versus 28 percent pre-COVID-19.

I often wonder and worry about a future where everything is digital. Change is never equitable, and especially the changes brought on by digital technologies and connectedness. Just as extreme poverty has been the outcome of industrial capitalism, we shouldn’t be surprised by technological inequity becoming a significant issue in the intelligence age.

We can already see this issue emerging in the pandemic. How often have you seen images of kids sitting in the parking lots of fast-food restaurants to access WiFi and attend their classes over Zoom? The Federal Communications Commission says that over 21 million people in the U.S. lack high-speed connectivity, though it should not be surprising that this is most likely a significant undercount. BroadbandNow puts the number at 42 million. Microsoft argues that 157 million Americans don’t get broadband speeds, even those with connectivity.

I find the Microsoft calculation to be the most compelling. The FCC defines broadband as minimum download speeds of 25 megabits per second (Mbps) and minimum upload speeds of 3 Mbps. Trying doing Zoom calls at that speed with a couple of kids and someone working from home. It is a ludicrous situation, especially since companies like AT&T are trying their best to shut down lower-priced DSL services without providing real affordable upgrade options.

A report by the Kansas City Fed found that almost 47 percent of adults making less than $30,000 a year don’t have broadband at home. Meanwhile, among those who have an annual income of over $75,000, only 5 percent don’t. And the majority of those without broadband at home live in rural communities. Another Kansas City Fed study from 2018 found that low-income households without internet access are much more likely to be unbanked. The lack of basic broadband connectivity is a problem that extends into everything, from education to health and money.

The rise of distance education, remote work, and telemedicine has made broadband a necessity. And nothing illustrates the need for connectivity more than a growing trend towards digital money. This shift is significant enough to be reflected in the stock prices of companies like PayPal, Square, Aydin, and others.

“Conventional banks now account for only 72% of the stock market value of the global banking and payments industry, down from 96% in 2010,” The Ecomonist reports. In the same story, they note, “The share of cashless transactions worldwide has risen to levels pundits had expected it to reach in two to five years. In America, mobile-banking traffic rose by 85% and online-banking registrations by 200% in the month of April.” Elsewhere, the magazine found that digital payments are up 52 percent at Venmo (part of PayPal) and 142 percent at Mercado Pago, a Latin American payment system.

According to a recent survey from 451 Research, contactless payments are here to stay.

- Two in five consumers are using cashless often

- One in three (29%) consumers said they increased their usage of contactless payments during the pandemic.

- Millennials (40%) and Gen X (39%) are the biggest contactless usage drivers.

- 86% of first-time users are going to stick with it.

I am a testament to this. I have been using the Apple Watch (Series 6) more often for contactless payments, and I have no intention or expectation of stopping. For those who don’t have or want an Apple Watch, more straightforward (and perhaps cheaper) devices are making their way into the market — for example, this one from Aeklys ring designed by Starck. The contactless credit cards are starting to become popular, and so are other new technologies. One example is the use of Amazon palm readers for checkout. As long as you have money and credit, you can find new ways to pay for things.

But what happens when you don’t have those luxuries? What if you are part of the global unbanked who rely on cash to get by? Given the sheer number of unbanked people around the world, what will be the societal ramifications of the mainstreaming of contactless payments? I know we aren’t there yet. We are going in that direction — and it will completely alter the idea of money as we have known it.

Whenever I think about digital change, I think about the camera. Not too long ago, we were married to the idea of a standalone camera and accustomed to its limitations. In came the smartphone, and it made us rethink what a camera is and what it can do. Subsequently, it has become the tool with which we capture and construct our daily reality. And it also has become a weapon of mass surveillance.

I see a lot of change happening during the pandemic (how we make payments being just one of them) that will upend our behaviors and change us as a society sooner than we may have expected. Some are already reaping the benefits of this transition, while others are already being left behind. The earlier we can identify the inequities created and exacerbated by the coming revolution, the greater the odds that we might actually address them.

Money is changing. We just need to prepare for it. Fast.