The Debt Beneath the Dream

Every gambler knows that the secret to survivin’

Is knowin’ what to throw away and knowing what to keep

‘Cause every hand’s a winner and every hand’s a loser

And the best that you can hope for is to die in your sleep

Kenny Rogers, The Gambler.

I don’t know Masayoshi Son, and I don’t need to. But my guess is that the SoftBank founder and CEO can’t be having a good start to his week. The stock of his flagship, SoftBank, is deflating faster than a balloon stuck in powerlines after a New Year’s party. He has bet big on OpenAI as his all-in wager. Whether he is right or wrong remains to be seen.

SoftBank’s shares dropped as much as 12.5 percent. Reports emerged that OpenAI and Oracle had scrapped plans to expand a flagship data center in Texas. Bloomberg reported the expansion fell apart over a combination of financing difficulties and shifting demand. The news undermines two core assumptions behind the entire Stargate Project. That alone should be reason to dig into every data center announcement and follow the money trail.

SoftBank’s credit default swaps widened. In plain English, the bond market is now charging more to insure against the possibility that SoftBank cannot pay its debts. The people who lend SoftBank money are getting nervous. Not a big surprise.

S&P, the credit rating agency, which already had SoftBank at junk, cut its outlook to negative earlier this month. A downgrade could raise borrowing costs precisely when SoftBank needs to borrow more than ever. These are legitimate problems. It also makes you wonder how SoftBank will meet its commitments to OpenAI in April 2026. I wrote about this last week, but even I didn’t know how much was up in the air.

I often refer back to my essay, The Announcement Economy, mostly because that is what we are living in. The details get lost in the bombast of headlines, and the media herd moves on to the next thing. Meme is the news, if news itself isn’t the news.

Let’s turn back the clock to January 2025. Stargate was announced with pomp and show that could rival Mardi Gras. President at the podium, Son and OpenAI’s Sam Altman flanking him. Big words, bigger promises. The beautiful future. Elon Musk, seemingly a sore loser for not being invited to the party, didn’t like it a bit. He said SoftBank “has well under $10 billion secured.” Altman fired back, called him wrong, and invited him to the Texas site. That Texas site is now the one being abandoned. Musk had obvious self-interest in undermining the project. He was also, turns out, right.

This is a good time to ponder the overall data center announcement frenzy. There is a level of insanity in all the news that keeps coming, and it deserves its own moment of skepticism.

I just read this New York Times piece about Nscale, a UK-based data center startup founded in 2024 that just raised $2 billion at a $14.6 billion valuation, with Nvidia backing and Sheryl Sandberg, Nick Clegg, and Susan Decker joining the board. The company barely existed two years ago. Its founder previously sold health supplements and worked in coal mining. Now he’s building “the engine of superintelligence.” Haven’t we seen this movie before? Different cast, similar theme with a charming, charismatic fundraiser and a board with more white shoes than an NBA star. Read the story and decide for yourself.

The irony of the name should not be lost on anyone. In model railroading, N-scale means 160 times smaller than the real thing. The real thing being a hyperscaler like Google, whose CEO told investors the company plans to spend up to $185 billion on infrastructure in 2026.

The data center buildout echoes the late 1990s fiber frenzy. Companies strung cable across continents for bandwidth nobody needed, on the assumption that demand would only go up and that the underlying technology would not change fast enough to matter. Both assumptions proved wrong. The chips will get faster. The models will learn to do more with less. The Excel chart pointing up and to the right rarely survives contact with Moore’s Law.

These are physical products, as much as they might seem like digital ones. You can’t put up walls faster than a query on ChatGPT. Neither can you get energy sources revved up on demand. Physics is physics, and atoms are atoms. It just doesn’t make for a good announcement.

Nscale is a UK company. Like everyone else, the UK is feeling left out of the AI buildout frenzy. Just like they did in the fiber buildout days. Don’t be surprised if you see more such announcements about upstarts raising billions from other parts of the world. No one wants to be left out of the announcement party.

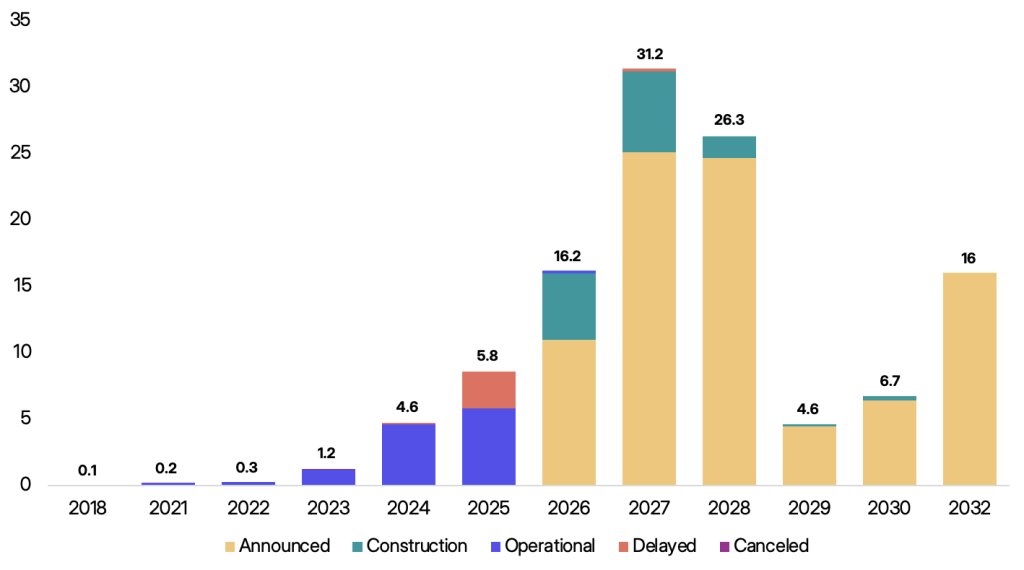

The scale of the announcements is staggering. US data center construction starts hit $77.7 billion in 2025, a 190 percent increase over the prior year. The four largest hyperscalers are on track to spend north of $500 billion on infrastructure in 2026 alone. But announcements and reality are two different things.

The numbers bear this out. I recently pointed to a report by Sightline Climate that is tracking 190 gigawatts across 777 large data centers announced since 2024. As I noted in a recent post, of the 16 gigawatts slated to come online this year, only 5 gigawatts is actually under construction. Last year, 26 percent of expected capacity slipped. Sightline’s estimate is that 30 to 50 percent of the 2026 pipeline won’t materialize. Look, if hyperscalers are building their own data centers, we know they can. They have the money. They have customers. They have the domain expertise. They can even spin up their own power sources. Others feel more like Milli Vanilli. They sound good. But is it for real?

I am an AI believer. But boy, the green gas coming out of the announcement engine makes me blanch.

If you see skepticism in my recent writing about physical infrastructure, it’s because sometimes you have to follow the dollars. In my earlier pieces on the $110 billion funding round and the announcement economy, I laid out how the headline numbers didn’t really add up. The structure hasn’t changed. SoftBank is seeking a new $40 billion loan, the largest dollar-denominated borrowing in its history, to meet its OpenAI obligations. Son is doubling down.

To fund the earlier rounds, Son sold SoftBank’s entire Nvidia stake for $3.3 billion. Those shares would be worth well over $150 billion today. He traded one of the great unrealized gains in modern investing history for a 13 percent stake in a company that remains unprofitable, whose flagship data center partner just backed out citing weak demand, and which S&P now considers a liability on SoftBank’s own balance sheet.(1)

Son may still be right. Yahoo Japan, Alibaba, ARM. He has been early and right before. He has also been early and spectacularly wrong — see WeWork. But the structure underneath, borrowed money, illiquid assets, a portfolio more than half locked up, means the margin for error is far thinner than any announcement headline ever suggested.

It isn’t money until it’s money. And it isn’t infrastructure until someone actually needs it. Uses it. And pays for it. As Kenny Rogers put it:

You got to know when to hold ’em, know when to fold ’em

Know when to walk away and know when to run

You never count your money when you’re sittin’ at the table

There’ll be time enough for countin’ when the dealing’s done

Footnote #1 (added on 3/10/26): I can see how my awkward sentence gives an impression that Son’s Nvidia sale funding OpenAI. The point I was making was that he has hyperactive style of a a gambler, and this is how he has ended up with OpenAI, and not with $150 billion if he knew how to hold them. Clearly my sentence structure could have been better.

Why I wrote this piece

- SoftBank’s bet on OpenAI is starting to weigh SoftBank’s shares have nearly halved in four months as questions grow over the scale of its OpenAI exposure. The FT’s Lex column has some strong words. (FT)

- SoftBank Seeks Record Loan of Up to $40 Billion for OpenAI Stake The largest dollar-denominated borrowing in SoftBank’s history, a 12-month bridge loan underwritten by JPMorgan and others, to fund commitments already made. (Bloomberg)

- The AI Data Center Boom’s Newest Billionaire Nscale, founded in 2024 by a former health supplements seller and coal miner, just raised $2 billion at a $14.6 billion valuation with Sheryl Sandberg, Nick Clegg, and Susan Decker on the board. The Times loves an outsider-looking-in story. (New York Times)

March 9, 2026

I would love to know why people with money think Son is some kind of genius. He hit a short-term gusher with Sprint but never followed up. Then he dumped a load of his Vision Fund into WeWork and similar crap. Now he’s taking the dregs of AI (OpenAI). This is not going to end well.

Yup, pretty much. He is a momentum investor who gets it right enough times that people keep giving him their money to gamble with.

Great points about AI financing. But one point needs some clarification.

“To fund the earlier rounds, Son sold SoftBank’s entire Nvidia stake for $3.3 billion. Those shares would be worth well over $150 billion today. ”

You may be conflating 2 separate Nvida sale and purchases by Softbank. According to this CNBC article, https://www.cnbc.com/2025/11/11/-sells-its-entire-stake-in-nvidia-for-5point83-billion.html:

Softbank first acquired Nvidia stock in 2017 and then sold it in 2019, which was before Open AI.

Softbank then reacquired Nvidia stock starting in 2020, which is what they sold in November. https://www.nasdaq.com/articles/why-did-softbank-just-sell-its-entire-nvidia-stake#:~:text=SoftBank%20Group%20(OTC:%20SFTBF),a%20total%20of%20$5.83%20billion.

So they did get the upside from 2020 to 2025, which was substantial.

None of the above changes the validity of the issues you raise about Softbank going forward. But we should make sure that we are following the complete money trail.

I am actually not conflating that point. I made the points you bring up in my previous piece, linked already. Son does have a history of getting in early and sometimes getting impatient. This has been a pattern.

Updated the piece to reflect my intent and that it is a poorly worded sentence.

Thanks Om – big fan. As you pointed out , Softbank’s had a very mixed track record. I recall them talking about a “300 year vision” of exponential technology growth back when they launched that Vision Fund, but then somehow they ended up missing the GenAI boat.

That being said, I think the recent revenue acceleration of Anthropic and OpenAI (an astonishing ~$44bln now vs ~$29bln in December) – makes me quite bullish on the industry’s growth prospects. Additionally, their cash positions post recent rounds should actually be quite strong (e.g., OpenAI disclosed $40bln in cash on hand as at Dec’25). The market is actually underestimating the labs’ financial firepower and traction. Instead of fearing for Anthropic and OpenAI’s sustainability – the market should be more worried about legacy platforms/walled gardens – AI will weaken those moats. Cheers

SoftBank made a mistake of selling the 2017 nvda stake early in 2019. But the sale that was done to fund the openai stake was different and the sale price was similar to current prices. So the opportunity cost of investing in openai was not $150bln like you mentioned. Would have been minimal given Nvidia shares have lagged since that Oct 2025 sale.

Pranoy

I see the sentence, and I really wish I had structured it better. It is convoluted at best and misleads and misrepresents my argument.