The Rocket That Runs on Broadband

SpaceX is in the business of rockets — how often they fly and what they do. The rest is imagination. The SpaceX IPO is a masterpiece of financial engineering. The prospectus is a perfect blend of reality, sci-fi, and skullduggery. I dug into the freshly filed 300-page IPO prospectus of Space Exploration Technologies Corp. to find out how much imagination is required.

SpaceX is seeking a valuation of $1.75 trillion, the largest IPO in American history, larger than anything Wall Street has previously been asked to absorb. In inflation-adjusted terms, SpaceX alone would rank second in history, just behind Saudi Aramco. SpaceX, OpenAI, and Anthropic together would raise more money than the entire dot-com bubble from 1995 to 2000.

Financial analyst Paul Kedrosky has a warning about where the money comes from. Most of that money will come from existing holdings. Passive funds will be forced buyers the moment these names enter the indexes, which index rules now accelerate. That means mechanical selling pressure on the same large-cap technology stocks everyone else already owns. Our 401(k) plans are in for a rude awakening.

Despite all that, I found the filing fun to read. It was late at night, so there was no popcorn. And who doesn’t like a bit of fiction before falling asleep?

The filing ranges from reusable rocket economics to the philosophical implications of becoming a Kardashev Type II civilization. It lists Mars colonization as a business line. I chortled when I saw that their flagship data center is named COLOSSUS, as in the 1970 sci-fi film Colossus: The Forbin Project, about a supercomputer that achieves self-awareness and takes over the world. To troll Microsoft, they have “Macrohard,” a platform under development to emulate digital workflows and create a fully AI-operated software company. If you want to know what a terawatt is, it is in the glossary. This is glorious.

Strip the prospectus to its financial skeleton and what remains is a satellite internet company. That is the business generating the cash that keeps the fiction appearing realistic.

One business that works

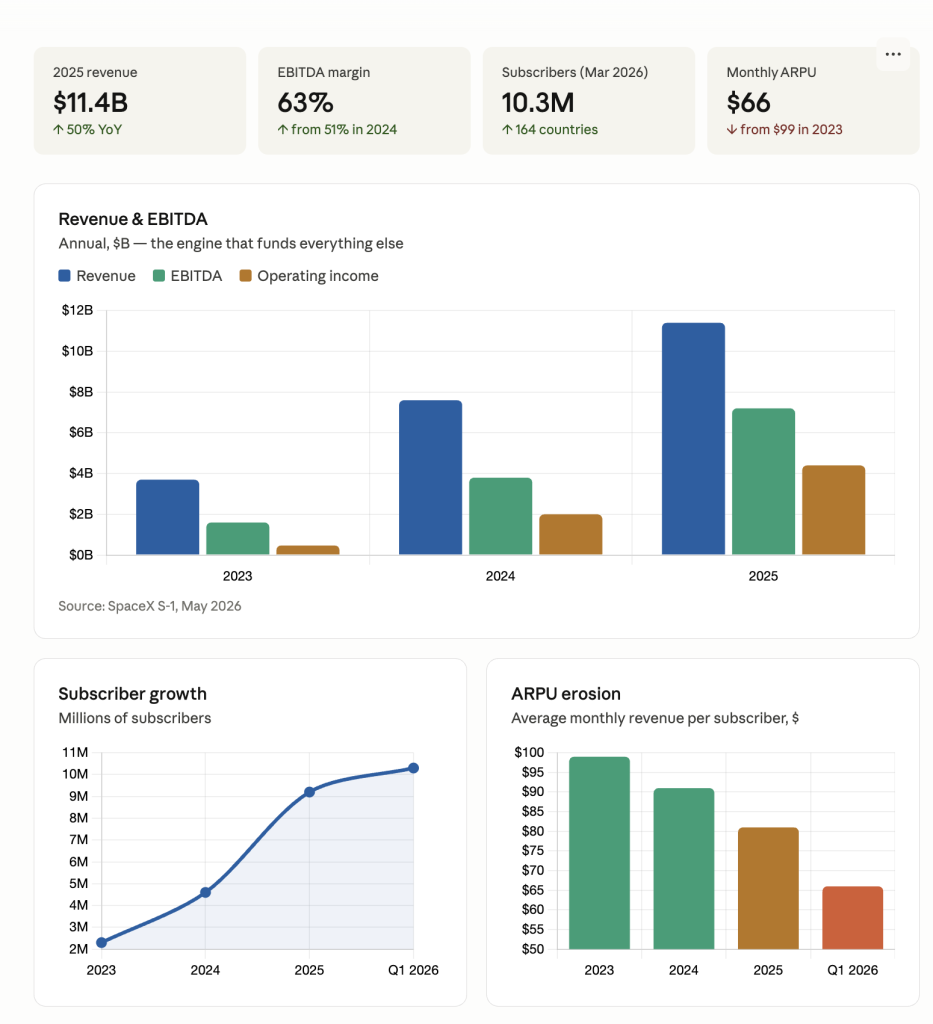

Starlink generated $11.4 billion in revenue in 2025. Operating income was $4.4 billion. Adjusted EBITDA was $7.2 billion, a margin of 63%. Revenue grew 49.8% year over year. Operating income more than doubled.

Comcast, providing cable broadband to 32 million American subscribers for decades, runs EBITDA margins in the mid-30s. AT&T is around 35%. Starlink, which commercially launched its first satellite in 2020, is running circles around both. It is not fiber broadband, but it is not selling that anyway.

The service had 2.3 million subscribers at end of 2023. By end of 2024, 4.6 million. By end of 2025, 9.2 million. The S-1 discloses 10.3 million subscribers as of March 31, 2026, across 164 countries. In November and December 2025, Starlink was adding 20,000 new customers per day.

How Starlink’s network economics work

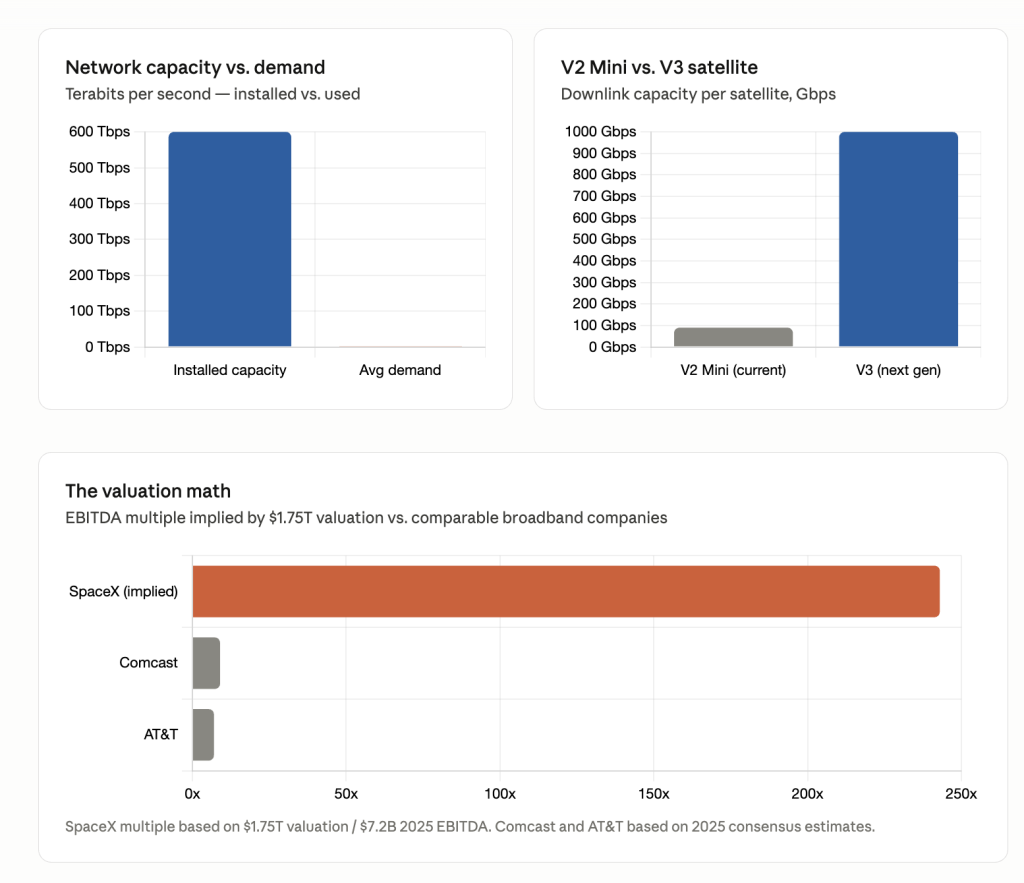

By end of 2025, the Starlink constellation had surpassed 600 terabits per second of network capacity. In 2017, the entire global public internet carried roughly 600 to 700 terabits per second. Starlink has now installed equivalent capacity at 25.7 milliseconds of median latency for American users.

For now, Starlink’s workhorse satellite is the V2 Mini. Each delivers approximately 90 gigabits per second of downlink capacity. A Falcon 9 carrying 22 of them adds roughly 2 terabits per second to the network at a marginal launch cost of around $30 million, about $15 million per terabit of installed capacity. Each booster reuse drives that lower. Once the satellites are in orbit, the marginal cost of carrying one more gigabyte approaches zero. Every new subscriber is nearly pure revenue.

The 10.3 million subscribers draw around 1.4 terabits per second on average. Against 600 terabits of installed capacity, that is a utilization rate of one quarter of one percent. Broadband networks are engineered for peak simultaneous demand, not average, so the number is low by design. But it also explains the margin.

The business has added 8 million subscribers in three years and lost one third of its per-customer revenue in the process. Total revenue keeps rising because volume growth overwhelms the price decline, but ARPU’s direction is a trend, not a rounding error.

The customer mix explains it. Maritime terminals (shipping vessels, oil rigs, research ships) pay between $250 and $5,000 a month and have no alternative. Aviation is even richer: a commercial aircraft terminal runs $12,500 to $25,000 per month. These customers anchored Starlink’s early ARPU.

Consumer residential is where the growth is now. It is the lowest-paying tier and, outside North America, increasingly price-sensitive. Add satellite-to-mobile users via carrier partnerships at a fraction of direct subscription revenue, and the mix explains the slide from $99 to $66 in three years. Maritime and aviation grow slowly and pay well. Consumer grows fast and pays less each year.

The question is where ARPU stabilizes. A lot of the world’s remaining unconnected population cannot easily afford $66 a month. African buyers are not the same as American buyers.

Starlink’s $7.2 billion EBITDA against a $1.75 trillion implied valuation is 243 times. That multiple needs ARPU recovery, subscriber growth, and a satellite generation that costs less to run.

Starlink needs the V3 satellites to work, . Each V3 satellite delivers more than 1 terabit per second of downlink capacity, against 90 gigabits on the V2 Mini. Each Starship launch carries 60 of them, adding 60 terabits per second in a single flight, more than 30 Falcon 9 launches with V2 Minis combined. A single Starship mission adds more capacity than the entire constellation did in its first year of commercial operation.

Upload matters too. The network currently delivers 225 megabits down and 20 to 40 megabits up. Each V3 satellite delivers 200 gigabits per second of uplink capacity, 24 times the current generation. Upload speed is what enterprise customers (large file transfers, remote operations, video production) actually need. V3 is the path back to high-ARPU segments and a valuation multiple that doesn’t require prayer.

The architecture around the engine

SpaceX absorbed xAI and Twitter into its financial statements before filing, treating all three as if they were always one entity. Twitter’s legacy debt, xAI’s $6.4 billion annual operating loss, and AI compute spending at $12.7 billion in capital expenditure in 2025 now sit on the same balance sheet as Starlink’s cash flows. The public investor buying Class A shares gets exposure to all of it, with no ability to elect the board or influence which claim on Starlink’s cash comes first. Too bad, because Starlink in itself is such a great business story. And I won’t get into who has ruined the skies above us for astronomers.

Analysts project Starlink revenue at roughly $20 billion in 2026. At sustained 60-plus percent margins, that is approximately $12 billion in EBITDA. Possible, but it requires Starship and V3 to work and growth in markets where $66 a month is already a stretch.

Starlink has brought real broadband to places that had none and built a moat on orbital slots, spectrum licenses, ground infrastructure, and manufacturing scale. None of it can be replicated the way software can.

At $1.75 trillion, SpaceX is asking investors to price in the orbital data centers, the Mars missions, the chip manufacturing, and the plan to build the infrastructure of a Type II civilization. The believers won’t know the difference. The faithful have been well rewarded before. They have also, occasionally, learned that their messiah is known to blow air hotter than the exhaust of those rockets.

May 21, 2026