Intel's dilemma and the slowly crumbling PC ecosystem

For an industry whose lot in life is to invent the future and challenge the status quo, technology’s giants are astonishingly stubborn when faced with change. And no two companies personify that more than Microsoft (s MSFT) and Intel (s INTC) — the glimmer twins of the personal computer revolution. For decades the PC buying cycle left these two companies sitting on a mountain of cash higher than even the highest Himalayan peaks. I guess when you are sitting at such heights, it is hard to look down and recognize that the base is being chipped away.

To be sure, I am not saying that Microsoft and Intel are going to go away tomorrow. Their fiscal muscle is enough to put even Popeye to shame. And monopolies (even quasi-monopolies) take forever to fade.

To be sure, I am not saying that Microsoft and Intel are going to go away tomorrow. Their fiscal muscle is enough to put even Popeye to shame. And monopolies (even quasi-monopolies) take forever to fade.

But for the first time they are facing a challenge that is much more profound and broader than they have ever faced in their monopolistic lives: competition and changing tastes. How they deal with these changes is going to write the next chapter of their corporate history.

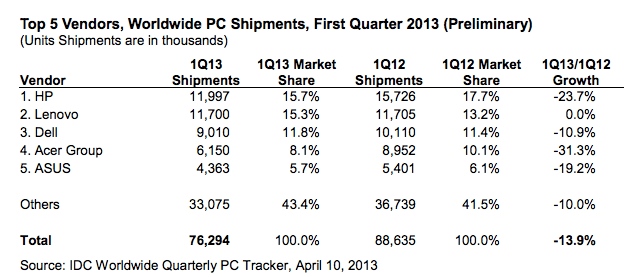

PC sales horror show

But let’s take a step back. The signs of crumbling came last week when research companies like IDC and Gartner shared data that showed double digit percentage declines in PC sales during the first quarter of 2013. To be sure, the first ninety days of the year are relatively slow for sales of consumer goods, considering that people go on a buying binge during the holiday season, but still a 14 percent year over year decline during the quarter is not something to skim over. It was so bad that even downward trend defying Apple (s AAPL) PC sales are expected to head south.

Many media reports blamed the Windows 8 operating system for this debacle, but this is the fourth quarter in a row we have seen PC sales sagging; we can’t blame the new operating system. The reason why media and analysts continue to make that correlation is because we have in the past made that correlation: new Windows equals big PC sales, almost like clockwork every three or four years. Except now it is not true because our relationship with PC (as we knew it) has changed.

The new personal

It has been just about six years since Apple’s (s aapl) iPhone launched and changed our expectations of computers and our relationship with technology. It became more intimate and personal than either Intel or Microsoft had imagined. It wasn’t as that the companies were unaware of mobile phones, or that iPhone was the first smartphone — Nokia and Palm had been selling them for quite a few years — but the iPhone and later Android phones became truly “personal.”

They made us spend less and less time on our PCs. They were always there, and even when the PC sat on the table, the phone in your hand was more fun and easy to use. And then three years ago came the iPad (and later other tablets) to take away even more of our attention from the PC. And when the iPad launched, I knew my PC was going to become less important. The iPad was my slate of imagination.

In the end, an increasing number of people are finding that they don’t need a whiz-bang PC anymore and they don’t need to upgrade because they can do a lot of things on their iPad or Kindle Fire or Samsung Android tablet.

The signs of this change were obvious to anyone who was paying attention. When Apple dropped “computer” from its name, the late (and then chief executive) Steve Jobs pointed out that it was a sign of the times and where the world was going. Here is what I wrote then:

Apple is making the phone do all things a computer does – surf, email, browse, iChat, music and watch videos. Nary a keyboard or mouse in sight, and everything running on OS-X. While I am not suggesting that this replaces our notebooks or desktops for crucial productivity tasks, the iPhone (if it lives up to its hype) is at least going to decrease our dependence on it.

The future is here

Six years later, the world has really changed for the twin gods of the PC. Unlike Apple and Google, who have hitched their bandwagons to wireless devices, Microsoft and Intel are still weighed down by the legacy of their past. I mean, it is hard for Microsoft to look beyond the profits from Windows and Office. It will always look at the future through the lens of those two products. I have been suspect of Intel’s ability to come out ahead as well.

Intel, too, is so married to the idea of selling more expensive PC chips and silicon for servers that it doesn’t know how to readjust its focus and its fiscal models around a world that wants lower priced chips for a different and always shifting market. Since then the world has embraced the little pocket marvels with amazing speed and that in turn has unleashed a new cellphone economics. The mobile chips are getting faster and faster. And thanks to demand that far strips the demand of classic PC devices, they are getting cheaper.

Intel, too, is so married to the idea of selling more expensive PC chips and silicon for servers that it doesn’t know how to readjust its focus and its fiscal models around a world that wants lower priced chips for a different and always shifting market. Since then the world has embraced the little pocket marvels with amazing speed and that in turn has unleashed a new cellphone economics. The mobile chips are getting faster and faster. And thanks to demand that far strips the demand of classic PC devices, they are getting cheaper.

The mobile phone market is so big that it has attracted all sorts of chip makers into the business: Qualcomm (s QCOM), MediaTek and Nvidia (S NVDA) are some of the players in the mobile chip business that are relentlessly flooding the market with faster, cheaper and more powerful chips. They are being helped by ARM Holdings, (s ARM) which keeps beefing up its chip technology and expanding its possible uses by focusing on not making chips, but instead licensing chip designs to others like Qualcomm.

Intel has to react to these guys; not to Advanced Micro Devices, the perennial also-ran that was always weighed down with an anemic balance sheet and an inability to compete even when it had better chips. And we all know, Qualcomm is no AMD. MediaTek knows how to play the mobile chip game better than anyone else. What does Intel have to show for its mobile efforts?

Change is hard

A lot of noise – press releases, product releases and a handful of devices. Sorry, but I remain resolute in my belief that the company’s DNA is making this transition to anywhere computing very difficult. That inability to change is reflected in the company’s current dilemma over the chief executive position. In an article this week, The New York Times detailed the likely replacements for outgoing CEO Paul Otellini.

Analysts say the two top contenders to be Intel’s next C.E.O. are Brian Krzanich and David Perlmutter, who are close to Intel’s core business. Mr. Krzanich, Intel’s chief operating officer, oversees its fabrication facilities. Mr. Perlmutter, the chief product officer, oversees chip design. Renee James, the head of Intel’s software group, is considered a more remote chance to run what has long been a hardware company. And Stacy Smith, Intel’s chief financial officer, is well liked inside and outside the company, but like Mr. Otellini, lacks an engineering background, which diminishes his prospects.

Regardless of who becomes the new Intel chief, the problem is that they were all weaned on the classic PC business, one that is changing with the rise of smartphones and tablets and lower power anywhere-computing devices.

That said (and as my wise colleague Kevin Tofel continues to remind me), Intel is doing relatively well with its Atom lineup of chips and he feels it is one of the reasons why Microsoft RT on ARM devices is facing challenges.

That said (and as my wise colleague Kevin Tofel continues to remind me), Intel is doing relatively well with its Atom lineup of chips and he feels it is one of the reasons why Microsoft RT on ARM devices is facing challenges.

The full Windows 8 tablets that run on Atom processors priced at the same price as RT devices (and with the similar battery life) should give Intel some hope. However, their addiction to the PC-style model and hefty margins that come from being almost monopolistic are going to challenge Intel in the future. As I wrote in the past, companies are defined by their corporate DNA and that determines their outcome.

Microsoft too has similar challenges as it grapples with the idea of competition and a world it doesn’t and can’t control anymore. More on that another day, but in closing, I would like to repeat what I said at the start of this piece: the companies that spearhead the talk of disruption and innovation are the ones who are afraid to disrupt themselves.

Between Intel and Microsoft, Intel has the better chance of surviving the transition. It holds a key advantage over its rivals: it owns the process development technologies and manufacturing facilities, whereas its competitors are limited by the ability of companies like TSMC to bring on new process technologies and have to compete with each other (and Apple) for capacity. As Intel gets serious in mobile, I believe you’ll see much faster and lower power processors at better price points than what’s available today. It’s very similar to what happened in the transition from desktop to laptop. Intel was slow to move, but when they did, they eventually dominated the market due to their superior processing technology, processor knowledge and manufacturing prowess.

Greg Borodaty is quite right. The breathtaking Microsoft reversals, surprises and immense new challenges have not occurred overnight, or without management culpability. Those of us who were forced to contend with the legendary Microsoft arrogance in the 1990’s see its current situation with some irony.

As you’re saying, Intel’s biggest obstacles are the company’s DNA and the cost structure. The first one because it means Intel will still focus on doing things the “old way”, and until they adapt, it could be too late.

And the second, because Intel simply can’t survive in the consumer space (and probably even the server space later, if ARM catches up to them there, too) as long as they don’t adapt their business to be profitable on $20 chips.

Sure, Atom may be “okay” (it’s not great, certainly not enough to beat the best ARM chips out there), but that Atom business is currently subsidized by the much more profitable Core business. Even if Intel can’t stay competitive with ARM on performance/battery life, it’s going to be very hard for them to stay competitive on price.

As the ARM chips become faster and faster, Intel will need to either make Atom just as fast or faster (which then presents another problem – what happens to the Core business, if Atom undercuts it?), or make the Core chips as energy efficient as the ARM chips, which even if it were possible, they would still be several years away from achieving it.

But in both cases, Intel is not going to be profitable. If they continue with Atom, and end up virtually eliminating the Core chips from the consumer market, because they aren’t competitive on price, then Intel *as a company* will have to survive on $20 chips (actually I think Atoms are about twice that right now, so even Atom isn’t competitive on price with ARM chips).

And if they do get the Core chips to the ARM level in efficiency, that will also mean regressing or stagnating in performance for the “ultra-super-mobile” Core versions, or whatever they will call them. They’ve already showed a proof of concept earlier this year with that dual core 800 Mhz IVB chip (that still had 10-12W TDP I think). And if finally, the ultra-mobile Core chips are just as fast and efficient as ARM chips, they will still be $100+ chips, so again, Intel can’t seriously use that to compete.

So in the end, what might kill Intel is not the lack of technical expertise in the ultra-efficient chips, but the fact that they will have to lower the prices of their chips so much, that it may not be sustainable for the company – at least without dramatically slashes costs, salaries, and all the “bloat” from the company, so they can be just as “lean” as ARM chip makers.

Lucian,

Intel actually has an advantage over the other ARM companies in terms of pricing power. The reason is that Intel has its own foundries where as the ARM companies are fabless and have to pay companies like TSMC a lot of money to make their chips. TSMC has margins of 50%, its not cheap.

Intel not only has their own manufacturing but they are several years ahead in technology. This is a big advantage because it gives Intel a much higher yield on their chips. So, their cost per chip is lower because of the more advanced technology then on top of that Intel gets to keep the foundry margins for themselves instead of paying them to TSMC.

Also keep in mind that Intel doesn’t just make the chips. They make many different kinds of components. So while the chip itself may only be $20, Intel will also get money from the other components.

The foundry advantage that Intel has is applicable throughout their product lines. Those factories are not restricted to just one type of chip. They make chips for all kinds of uses. So when you look at market share as a factor driving down costs, you need to look at the entire picture. Its not just smartphones or tablets, it is smartphones + tablets + pcs + servers + embedded devices. That’s a lot of market share for Intel right off the bat even starting at low levels in smartphones and tablets.

Om, There is another trend, computing is going away from computers (things that need booting) towards appliances. People are just sick and tired of being constantly made aware of the short comings of the operating system. They prefer an invisible OS.

Om Malik’s post on Intel is a classic case of “visualizing” a glass half full or half empty. Other competitor bloggers have come to a much different conclusion, as recently as yesterday, based on the identical facts. As one blogger pointed out, Intel and IBM have a prestigious history of reinventing themselves over many decades by plowing money into R&D.. Another problem is seizing on short term Intel results. Peter Drucker is famous for saying, “long-term results cannot be achieved by piling short-term results on short-term results.”

Longer term, one speaks pessimistically about Intel at their own peril.

I don’t agree that Intel is in any kind of trouble. Intel makes chips and they are way ahead of competitors in their foundry capabilities. They just released a lot of new chips this year that will go into smartphones and tablets. In another year or two they will be able to put out chips using their 14nm technology. So I believe that Intel chips are going to be widely used in the Android market.

Intel also has a fantastic data center business which is growing very quickly. From what I understand for every six smartphones sold, in aggregate one server is needed to support them.

Also I would like to mention that even if Intel is never able to get business for Apple’s ios devices they would still have a huge opportunity to provide foundry services for Apple. Intel has the most advanced foundries in the world and Intel could make a lot of money partnering with Apple in this way. The other large foundries like TSMC have margins of 50% and their foundries are not as leading edge as Intel’s.

Intel had better hurry, once Apple gets the A-Series chips into the performance range of laptop and desktop computers look out.

Intel’s mythical fabrication advantages have largely been irrelevant in the market section that could most benefit from them: Mobile. Node shrinks are supposed to bring advantages in power consumption. At a full node advantage Atom = ARM in performance per watt. That’s kind of bad news since Atom was originally designed to use the spare capacity on older process nodes and maximize the revenue from those investments.

Also, we’re hitting diminishing returns on node shrinks. We’ve already seen that with the move to 22nm. With both a die shrink and the additon of a Finfet architecture, they barely managed to get half the advantages in speed and wattage that previous shrinks netted them. This may have been due to inefficiencies in the Ivy Bridge chip itself (likely induced by the lack of compitition in the x86 space), or an indication of other issues. From my understanding of the issue ever since 40nm, this has been an issue though with everyone, and can be seen from the modest gains in ARM and GPU architectures as they’ve scaled down, speed and wattage haven’t scaled down in the same ways they used to.

This means that increasingly the advantage to be had out of die shrinks is a minor performance bump, minor reduction in wattage, and the inevitable price advantages of squeezing more chips onto the same amount of silicon. However, as we move into needing hard radiation to do the lithography at increasingly smaller resolutions, those price advantages are being offset by tremendous R and D costs, as well as ramp up costs.

We’ll see what Haswell brings. But looking at the market form the outside, it certainly looks like Intel is getting to the point where the competition is able to reach ‘good enough’ faster than Intel can move the CPU performance ceiling. That plus decreased need for more CPU power in the consumer market means that for the first time, Intel is facing a market where it can’t just make a better product that consumers can’t live without. This time they face the very real threat of A) overserving the market, and B) facing disruption from below and on the side. The top of the market may be enough to keep them going, but probably not. Especially if they stumble, or their process advantage fails to net them actual benefits, in which case they could suffer the same fate that Intel inflicted on the Big Iron makers they displaced on their way to market dominance.

Intel is too big. Break it up. This idea will be as welcome as a skunk at a garden party. Break out some of the fabs, like AMD did. Slice the company horizontally, vertically, or both. Some parts won’t survive. This is key. Fear of failure is a great motivator, and Intel can’t see that happening from atop its huge pile of cash.

Roland, you said it right… the idea will be as welcome as a skunk.

I don’t see the PC disappearing any time soon – you just cannot replace serious hardware with a luxury toy.

Intel is in a much better position than Microsoft, they have diversified technologies and are not only dependent on the PC market. Currently the PC/Server market is their cash cow, but they can move into other areas as they have the know-how.

Microsoft is in a worse position, their mobile efforts is not yielding the results they hoped for, Windows 8 is not the big attraction they bargained on, and Azure not the trumpcard they bargained on.

Intel’s numbers came out yesterday. PCs are only down around 6% while servers are up 8%. The sky is not falling.

Intel put out 22nm Atom products this year. In another year or two they will have 14nm Atom chips. Intel will be a big player in smartphones and tablets within the next few years.

Just wondering company setup by Moore (law) and Andy groove (only paranoid can survive) , why had missed the boat and can’t cop up with changes?

It seems like we are entering a new era. The convergence of smartphones, tablets and video lliberated from legacy hardware and software have created the neXtWave.

I go for weeks without my laptop. Wondows did not help their cause with the confused Windows 8 platform. Apple’s laptops seem ridiculously overpriced for what they offer. Google seems to be closer to how our digital lives are unfolding.

Certsknly there will continue to be a market for laptops. Writing a novel on a smartphone is not practicable. But key market segments are abandoning phone companies, cable companies. The advent of Netflix and other on-demand video sources make older business models seem increasingly irrelevant. Netflix acquired more new clients than HBO. Even Verizon is experimenting with a newer business model.

The convergence of disparate devices poweted by incompatible operating systems able to combine data from all manner of devices. Cloud storage is eliminating the need to chose one type or format.

Intel’s market claiim is dwindling. As is Microsoft.

But as IBM showed jn their latest esrnings reports, good is no longdr good enough.

Whichever company or companies meet the needs of the convergence evolution will be the future the neXtWave web.

The reason for the shift into mobile devices can be also attributed to the availability of the cloud